A second day of losses throughout cryptocurrency markets is giving would-be traders a chance to buy that may not be repeated.

Bitcoin dropped below $10,000 on Cointelegraph’s price index Wednesday, Jan. 17. On the same day, Ethereum (ETH) went below $900, marking a price slide of over 30% for both assets this week.

Bitcoin price chart (Image: geralt/Pixabay)

Community and industry figures have reacted with mixed emotions to the downturn, which mimics behavior seen in January over the past three years.

The price of bitcoin has fallen below $10,000 for the first time since early December.

According to CoinDesk’s Bitcoin Price Index (BPI), the cryptocurrency’s value has hit a low of $9,714.02 as of press time. The last time bitcoin’s price was below $10,000 was on Dec. 1, BPI data shows. Bitcoin Price Chart (Image: NikonD300/MaxPixel)

As of the time of writing, the price had recovered somewhat, trading at $9,737.20. Market analysis suggests that the price could shift in either direction and recent regulatory developments – out of South Korea and China in particular – could roil markets further, according to some observers.

Bitcoin’s come comes amid the backdrop of a wider fall in cryptocurrency markets, a state of affairs which was on full display during yesterday’s trading session. Data from CoinMarketCap shows that many of the top cryptocurrencies remain in the red for the past 24 hours, including ether, which has fallen below $900.

[No great surprise here – most people in the crypto community know BitConnect as a Ponzi scheme]

The company behind the controversial cryptocurrency BitConnect has announced that it will close down its lending and exchange platform.

BitConnect Home Page (Image: BIUK)

BitConnect’s lending service will be shuttered, effectively immediately, while its exchange platform will close in 5 days, according to a post on its website published Tuesday.

“In short, we are closing lending service and exchange service while BitConnect.co website will operate for wallet service, news and educational purposes,”

the post explained.

The announcement blames a myriad of factors, perhaps most notably the cease-and-desist letters issued in recent days from regulators in Texas and North Carolina.

Both letters stated that BitConnect was engaging in the sale of unregistered securities tied to a token sale.

“We have received two Cease and Desist letters, one from the Texas State Securities Board, and one from the North Carolina Secretary of State Securities Division,”

the BitConnect team wrote.

“These actions have become a hindrance for the legal continuation of the platform.”

The post also blamed “bad press” that has “made community members uneasy and created a lack of confidence in the platform.”

BitConnect has been accused of constituting a Ponzi scheme, and several figures in the space, including the founder of ethereum, Vitalik Buterin, have levied criticisms against it in recent months.

Bitcoin’s price has been on a wild ride since its inception.

2017 alone saw massive gains, starting the year at under $1,000 and, at its peak, breaking $19,000, according to industry site CoinDesk.

On Tuesday, it was trading at $11,943, a decline of 12 percent, according to CoinDesk.

As bitcoin’s popularity surges and its price rises and falls, more and more people are asking the same question: How does bitcoin, something that’s essentially invisible and intangible, have value?

Bitcoin Cryptocurrency (Image: MaxPixel)

Scarcity and utility

In economics, something has value if it checks the following two boxes: scarcity and utility. Scarcity just means that something has a finite supply. In the case of bitcoin, the cryptocurrency has a set cap of 21 million bitcoins.

Many analysts note that this set cap makes bitcoin more desirable than other assets, even gold. That’s because unlike with gold, there’s no need to worry about a digital Gold Rush. A treasure trove of bitcoin won’t ever be “discovered,” causing the crypto’s price to crash with an influx in supply.

“There are potentially millions of times more gold underground than actually has been extracted,”

said Tom Lee, head of research at Fundstrat Global Advisors. Lee was chief equity strategist at J.P. Morgan before co-founding Fundstrat in 2014.

The most watched Bitcoin introduction video ever. Updated in April 2014, this video explains how bitcoin works and the importance of this paradigm shifting technology.

The year of 2017 was a fantastic year for some Bitcoin users, but others were not so lucky with the cryptocurrency.

Below, we’ll look at some of the most impressive success stories of the year, as well as the profiles of people who probably wish they’d never touched Bitcoin at all.

It’s a highly erratic currency, but people who invested in it before its recent prominence often found their foresight was lucrative in ways they never imagined at first.

Bitcoin price chart (Image: geralt/Pixabay)

This Anonymous Person Who Became a Bitcoin Millionaire

One anonymous person who posted a detailed story on Steemit said that in 2010, the price of each Bitcoin was so low that it was not even valuable enough to buy a pizza. Still, by the end of that year, the person reportedly had 12,000 Bitcoins and collecting the large number of them paid off.

That’s because by April 2013, the worth of each Bitcoin had ballooned to over $100. Due to some issues in the individual’s personal life and a few other non-Bitcoin-related factors, the person took a couple of breaks from Bitcoin but was never completely out of the loop with them. Eventually, this anonymous Bitcoin user heard that the 12,000 Bitcoins were now worth over $10 mln.

Despite that fortunate turn of events, the person only began selling them in small quantities so as to not attract attention. The individual also planned for the future by choosing investment strategies and did not let the rapid wealth impact their employment. As words of advice, the person suggests exercising patience and not getting greedy, while also keeping up on newsworthy events.

Erik Fineman

Erik Fineman began investing in Bitcoins in 2011 when he was only 11 after his grandmother gave him $1,000 and his brother offered him a tip about what to do with the money. In those early days, Bitcoins were only worth $12 each. However, when Fineman sold his first Bitcoins at the end of 2013, each one had a value of $1,200.

The bitcoin price has dipped below $13,000 for the second time in December, following the December 23 correction which led the price of bitcoin to plummet to $11,500.

Bitcoin Dominance Index at 37.9 Percent

Analysts have attributed the recent decline in the price of bitcoin to the unexpected surge in the valuation of several cryptocurrencies including Ripple and Cardano.

Over the past 24 hours, the market valuation of Ripple has increased by nearly 100 percent, surpassing $100 billion in market cap. While it has corrected since then, the market valuation of Ripple still remains above $89 billion, more than $23 billion higher than that of Ethereum.

Apart from the one brief period in November during which Bitcoin Cash overtook Ethereum for several hours, Ethereum had not given up its position as the second most valuable cryptocurrency behind bitcoin throughout the past 12 months. Yet, Ripple remains as the second most valuable cryptocurrency behind bitcoin 24 hours after it has initially taken over Ethereum.

For the first time since June, the dominance index of bitcoin over the cryptocurrency market has dipped below 38 percent. At the time of reporting, the dominance index of bitcoin is 37.9 percent, and is close to achieving an all-time low at 37.39 percent.

Historically, bitcoin has demonstrated a trend in which the value of bitcoin surges when other alternative cryptocurrencies drop. In contrast, when the value of alternative cryptocurrencies decline, the value of bitcoin has tended to increase.

As such, given that the recent fall in the price of bitcoin was mostly triggered by FOMO or fear of missing out demonstrated by a small portion of bitcoin investors switching over to Ripple, the bitcoin price will likely be able to recover to the $15,000 relatively soon, especially if the market cannot sustain the valuation of Ripple at around $90 billion.

BITCOIN will be taxed following a dizzying year of price rises and falls, industry experts have warned as the volatile cryptocurrency continues moving towards the mainstream.

With bitcoin’s price rising 1100 per cent over 2017 the HMRC has decided against creating new legislation to ensure the investment gains are taxed appropriately.

But experts have warned the cryptocurrency will not remain exempt from tax.

Bitcoin Price Chart (Image: NikonD300/MaxPixel)

Benjamin Dives, CEO of London Block Exchange told Express.co.uk:

“In this world, nothing can be said to be certain, except death and taxes. Cryptocurrency may be new and unique, but it is not exempt from tax liability.”

Mr Dives says individuals who profit from their Bitcoin investments will be required to pay capital gains tax – just like those who profit from the disposal of their stocks, shares and other investment instruments – through their annual self-assessment.

Profits from bitcoin price rises are subject to 20 per cent Capital Gains Tax – or 19 per cent Corporation Tax if it’s a company doing the trading. Everyone has a Capital Gains Tax free allowance of £11,300 per annum – any gains up to this amount are tax free.

For most casual Bitcoin owners I would recommend the Electrum Wallet to hold their Bitcoin. However, many other wallets exist and here we’ll look at the Bitcoin Core one.

Bitcoin Core, as its name suggests, is maintained by the same team as the core Bitcoin software so you know it’s trustworthy. According to their website:

In addition to improving Bitcoin’s decentralization, Bitcoin Core users get better security for their bitcoins, privacy features not available in other wallets, a choice of user interfaces and several other powerful features.

For advanced users these additional features can be useful – for example I used Bitcoin Core to access the private keys for a Bitcoin address in Segwit format, something I couldn’t do with Electrum

There is a big obstacle to using the Bitcoin Core wallet, though, that one needs to be aware of: it requires downloading the entire Bitcoin blockchain to your computer. This can take a long time (for me, about 4 days) and use a lot of storage (a couple of hundred Gb).

First download the Bitcoin Core installer from the Bitcoin.org website, choosing the appopriate one for your system – Windows 64 bit for most people. Run the installer:

Starting the Bitcoin Core Installer (Image: BIUK)

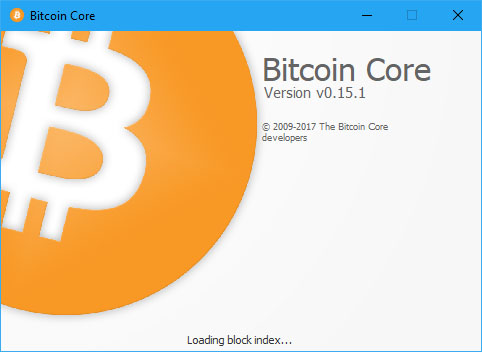

You will get the usual options for install folder, menu folder, etc. Once installed, run the Bitcoin Core program. It will start by saying it’s loading the block index:

Bitcoin Core loading index (Image: BIUK)

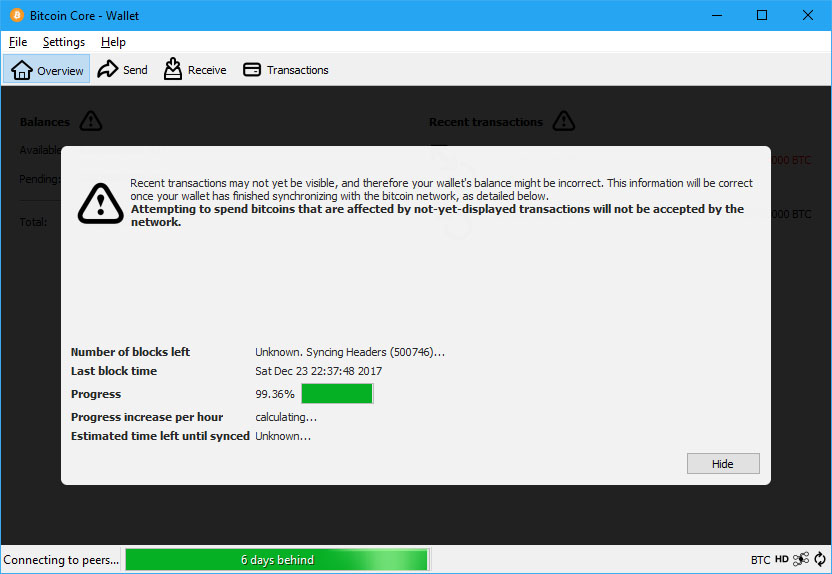

Then it will begin verifying blocks. Each of these operations can take some minutes to complete. It will then begin the synching of blocks:

Bitcoin Core synching blocks (Image: BIUK)

Very roughly you might find this takes about a day per year that you are behind since the creation of Bitcoin (so of course it’s a long time the first time, but much faster the next time you open it). If you need to you can close Bitcoin Core while it’s working and it will restart when you open it again – though of course that will extend the time it takes to synch.

Note that you can toggle the synch status display by pressing the right-most icon in the bottom status bar.

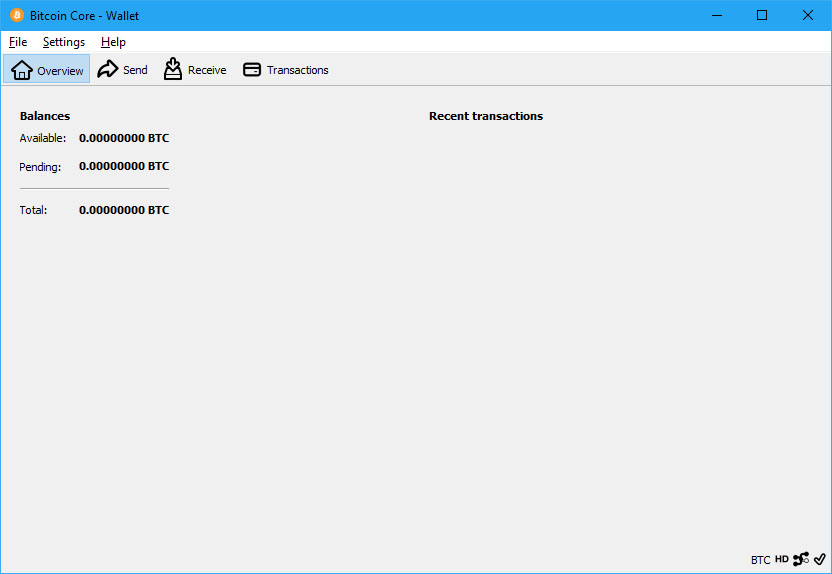

Eventually it will complete and you will be at the Overview screen, and the synch status button will be a tick:

Bitcoin Core Overview (Image: BIUK)

The wallet is now up and running and you can send and receive Bitcoin through it in much the same way as with the Electrum wallet previously described. Additional features will be covered in later posts.

The leading Bitcoin and Cryptocurrency site for UK investors