Bitcoin prices fell below $10,000 Thursday as a bear market reversed growth which saw BTC/USD achieve weekly highs of $11,675 March 5.

Price data from Coinmarketcap shows Bitcoin losing around $400 in three hours to hit $9658, recovering slightly to trade around $9900 at press time.

Bitcoin price chart (Image: geralt/Pixabay)

The behavior continues what has become a pattern for BTC/USD over the past month, with upticks towards $12,000 encountering resistance before diving below $10,000, then repeating the cycle.

As Cointelegraph reported previously, several analysts have warned that closing above $12,400 will be a decisive event for traders, but this will be difficult to achieve.

I was right about the Bitcoin Dip – and have made a tidy profit. I bought half a Bitcoin at £5500.

Of course, it should have cost me £2750 but I bought it through Coinbase with my debit card which is a pricey, though convenient, way to do it. Coinbase charged me 4%, so about £110, making the total £2850.

Bitcoin was been rising in value since as I predicted, though in its usual erratic way. I had intended to take my money out when it passed £8000 and, as I watched it last night, it did just that.

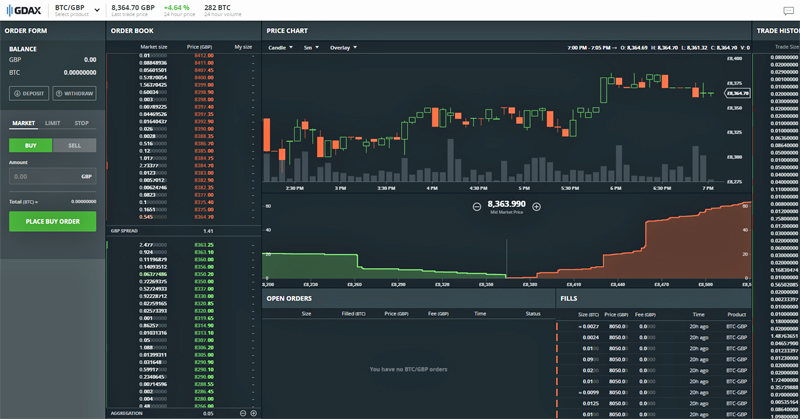

I was hesitant to sell it directly through Coinbase again because of its fees. However, I had come across some advice about selling through Coinbase’s exchange, GDAX, instead at lower fees. Here’s an example video from the excellent Coin Mastery:

I followed the advice and it worked like a charm.

GDAX Exchange Trading Screen (Image: BIUK)

This is the process if you want to save a stack on Coinbase fees:

Create a GDAX account if you don’t already have one (I already did).

Transfer the Bitcoin to GDAX – on GDAX click the DEPOSIT button, then in the form choose your Coinbase Account -> BTC Wallet and set the amount. Click Deposit Funds. It will appear almost immediately on GDAX and there is no charge.

Select LIMIT then SELL, then set the amount. Here you need to be a bit careful and set the correct price you are prepared to sell at (double check it, because if you set it low it will sell low). At the time Bitcoin was selling for about £8010. I wanted to make sure that, if there were fees, I would clear £4000 on my 0.5 BTC so I set the value to £8050.

Since the price is volatile your price will likely be hit very quickly so long as you didn’t set it too high (mine too less than a minute).

The BTC sells, the money appears in your GDAX wallet – and there’s no fee!

Transfer the money back to Coinbase using the WITHDRAW button, set the amount and the destination (e.g. GBP Wallet) and click WITHDRAW FUNDS. It goes back to Coinbase – no charge.

So I have proved to my own satisfaction you can sell BTC, i.e. convert it to pounds sterling, for no charge this way – and at a price slightly higher than the current market rate

Note that selling Bitcoin is called a ‘Maker’ transaction since you are putting Bitcoin into the market. Note that moving in the opposite direction has a ‘Taker’ fee of 0.25%, still not a bad deal.

I sold my 0.5BTC at £8050 so I received £4025, and that’s all now sitting in my Coinbase account.

Since I only paid £2870 for the Bitcoin less than a month ago (a profit of about £1100), I’m rather pleased with that.

After my initial experiments into mining for cryptocurrency with my own PC’s GPU and CPU, and even before acquiring my improved GPU, it was clear that good mining results were only possible with specialised and up-to-date hardware. Therefore about Christmas I ordered a new PC with a view to designing it for use in cryptocurrency mining.

We needed a new family PC for occasional use anyway (for children’s homework, etc.) as our previous one was old and had slowed down to the point it was almost useless. At the same time I knew it would be idle most of the time, when it could be used as a dedicated mining machine.

The Beast – High End Mining PC (Image: BIUK)

I took some time investigating the options before deciding on the specification I wanted. Although all our previous PCs had come from Dell, this time I ordered through Scan PC to get exactly what I wanted at an acceptable price:

A gaming motherboard with twin high speed GPU slots

A large, clear-airflow case with sound insulation

Two top-end GPUs – the NVidia GTX 1070 Ti

A high power (850W) power supply

High performance disks (an SSD for fast access, and a RAID array for backup)

The Beast – High End Mining PC (Image: BIUK)

In discussions with Scan I changed the spec a couple of times after ordering (e.g. increasing the memory) and was pretty happy with their service. It arrived in January and so far has shown itself to be a very powerful machine. It cost an eye-watering £2500, but then the two graphics cards alone were about £650 each.

I’ll blog about how I got on with it, including its mining capability, in the next few posts.

In January I completed and filed my 2016-2017 UK self-assessment tax return, for which I had to consider the tax implications of my cryptocurrency holding and trading. While I was able to convince myself that there were no issues for that period, since I had sold no cryptocurrency (only bought) in that period, it was clear that I would definitely need to consider tax in detail for the upcoming 2017-2018 period.

My first step, back last summer, was to invest in a cryptocurrency accounting app known as CoinTracking.info. I have used it carefully since to record all transactions, but nonetheless it was clear that while it could help with tax filing, it was necessary for me to research and understand the issues myself.

Bitcoin ‘Taxation is Theft’ (Image: Pixabay)

The tax situation in the UK for cryptocurrency is unclear so here I’m going to record my views on the current situation – if anyone knows otherwise, please detail any corrections in the comments.

In a nutshell for an individual (not a company) with a moderate amount of cryptocurrency (less than £45k) it is as follows:

Capital Gains Tax (CGT): If you buy and sell cryptocurrency then you are liable for capital gains tax on the difference in value of the currency between when you bought it and when you sold it, valued in pounds sterling. Where this exceeds the CGT tax-free allowance (£11,300 for 2017-18) there is tax to be paid.

Income Tax: If you trade or mine cryptocurrency then you are liable for income tax on the value of the currency gained, valued in pounds sterling. Where this exceeds the income tax personal allowance (£11,500 for 2017-18) there is tax to be paid.

Value Added Tax (VAT): In virtually all circumstances VAT can be ignored (as with most conventional currencies).

While the guidance suggest that on a case-by-case basis some cryptocurrency transactions may be considered to be gambling or betting – and therefore not taxable – I will assume that the safest course is to assume that, if reviewed, all transactions will turn out to be taxable on the basis just described.

Note that, in my opinion, income tax is probably liable on any free gains of cryptocurrency, for example:

With regard to CGT, it looks like cryptocurrency will be valued in the same way as shares. If you have bought and sold lots at different times then the value of what you sell compared to what you paid for it can be difficult to calculate – how do you match which sold Bitcoin to which bought Bitcoin?

Following HMRC guidance for shares the process is basically:

Same Day Rule: If you buy and sell on the same day then the coins can be matched off against each other (even though you bought and sold at different values) and there is no CGT liability. You just have to consider CGT on any ‘left over’, i.e. if you sold more than you bought.

Bed and Breakfasting Rule: Any coins not covered by the first rule but bought and sold within 30 days can be matched against each other, and CGT is due on the difference between the buying and selling values.

All others: Any coins not covered by the first and second rules are considered to be held in a single pot (called a ‘Section 104’) and when some are sold they are valued at their proportion to the value of the total pot. That value is determined by adding up the bought price of the coins in the pot.

That’s the tax situation for cryptocurrency as I understand it so far, though of course I will look into it further in time for my next tax return. With that return in mind, I have decided to do some specific bookkeeping in advance (probably in spreadsheets) and if you own crypto you might want to consider doing something similar:

Track the buying and selling of all crypto coins to pounds, with dates, in order to determine the CGT liability as per the 3 rules just described.

Track the receipt of any free coins (including airdrops, forks and faucets) in order to determine the income tax liability – even if (particularly if) the coins ended up in the same account as those that were paid for.

Bank of America (BoA) has admitted to US regulators it may be “unable” to compete with the growing use of cryptocurrency.

In its annual report to the Securities and Exchange Commission (SEC) this week, filed Feb. 22, the major US bank for the first time highlights cryptocurrency as an area that may cause it “substantial expenditure” as it tries to remain competitive.

“Our inability to adapt our products and services to evolving industry standards and consumer preferences could harm our business,” BoA states in the filing.

As banks worldwide eye the cryptocurrency phenomenon, direct interaction remains low. The lack of uptake formed a central reason why the European Central Bank confirmed it had opted for a hands-off approach to legislating the area earlier this month.

Open bank vault (Image: ahobbit/Pixabay)

While BoA has sought to innovate in the sphere, receiving a patent for its proposed cryptocurrency exchange system in December 2017, it has come in for criticism more recently after blocking its clients from credit card purchases of cryptocurrency.

Seven of the largest crypto companies are forming a UK cryptocurrency trade body, bringing in the first self-regulation for the wild west sector worth £290 billion.

CryptoUK, whose members include the popular Coinbase exchange and trading platforms eToro and CryptoCompare, said it had produced the first code of conduct for the industry to abide by.

The companies said they hoped the regulations would form the first part of broader UK rules around volatile cryptocurrency trading.

Cryptocurrency Art Gallery: Litecoin, Ether, Ripple, Bitcoin and Namecoin (Image: Namecoin/Flickr)

Bitcoin’s rise last year has made it a popular phenomenon, with its value increasing to as much as $20,000 (£14,400) in December, before falling below $7,000 last week. While Bitcoin has made made some millionaires it has left many amateur investors out of pocket, while others have fallen victim of cryptocurrency scams.

CryptoUK chair Iqbal Gandham said there was a risk of “rogue operators”, but the new body had been established “to promote best practice and to work with government and regulators”.

Analysts are concerned that Bitcoin and cryptocurrency mining centers are spending too much electricity, and that the process of verifying cryptocurrency transactions could worsen the global environment.

Justification of mining in Bitcoin and cryptocurrencies

In December 2017, several analysts criticized the electricity consumption of Bitcoin and cryptocurrency mining centers, calling the mining process an “environmental disaster.” Earlier Cointelegraph reported that cryptocurrency mining will likely exceed electricity consumption of households in 2018.

Cryptocurrency Mining Farm (Image: M. Krohn/Wikimedia)

Smari McCarthy of Iceland’s Pirate Party stated that excessive consumption for Bitcoin mining is not practical because the main use case of Bitcoin is for “financial speculation.”

“We are spending tens or maybe hundreds of megawatts on producing something that has no tangible existence and no real use for humans outside the realm of financial speculation. That can’t be good.”

If environmentalists and analysts perceive the main use case of Bitcoin and other cryptocurrencies to be financial speculation, the consumption of a massive amount of electricity could be considered impractical. However, the main application of Bitcoin is not financial speculation. In countries wherein the underbanked struggle to gain access to financial services, Bitcoin operates as an efficient currency.

In Venezuela, for instance, local residents are using Bitcoin to order food, basic goods and medicine from outside of the country because the Venezuelan bolivar, the country’s national currency, has lost almost all of its value, and has become virtually worthless.

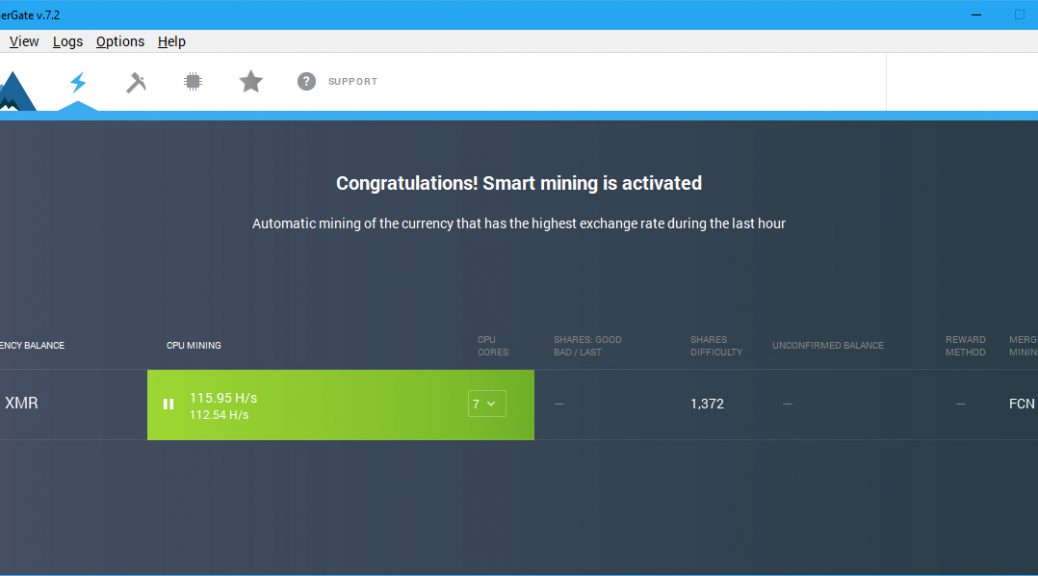

My recent attempts to mine cryptocurrency using CCMiner and MinerGate were disappointing dead-ends – I had really been sidetracked by accounts I’d read of people making these approaches profitable, even though they were not mainstream.

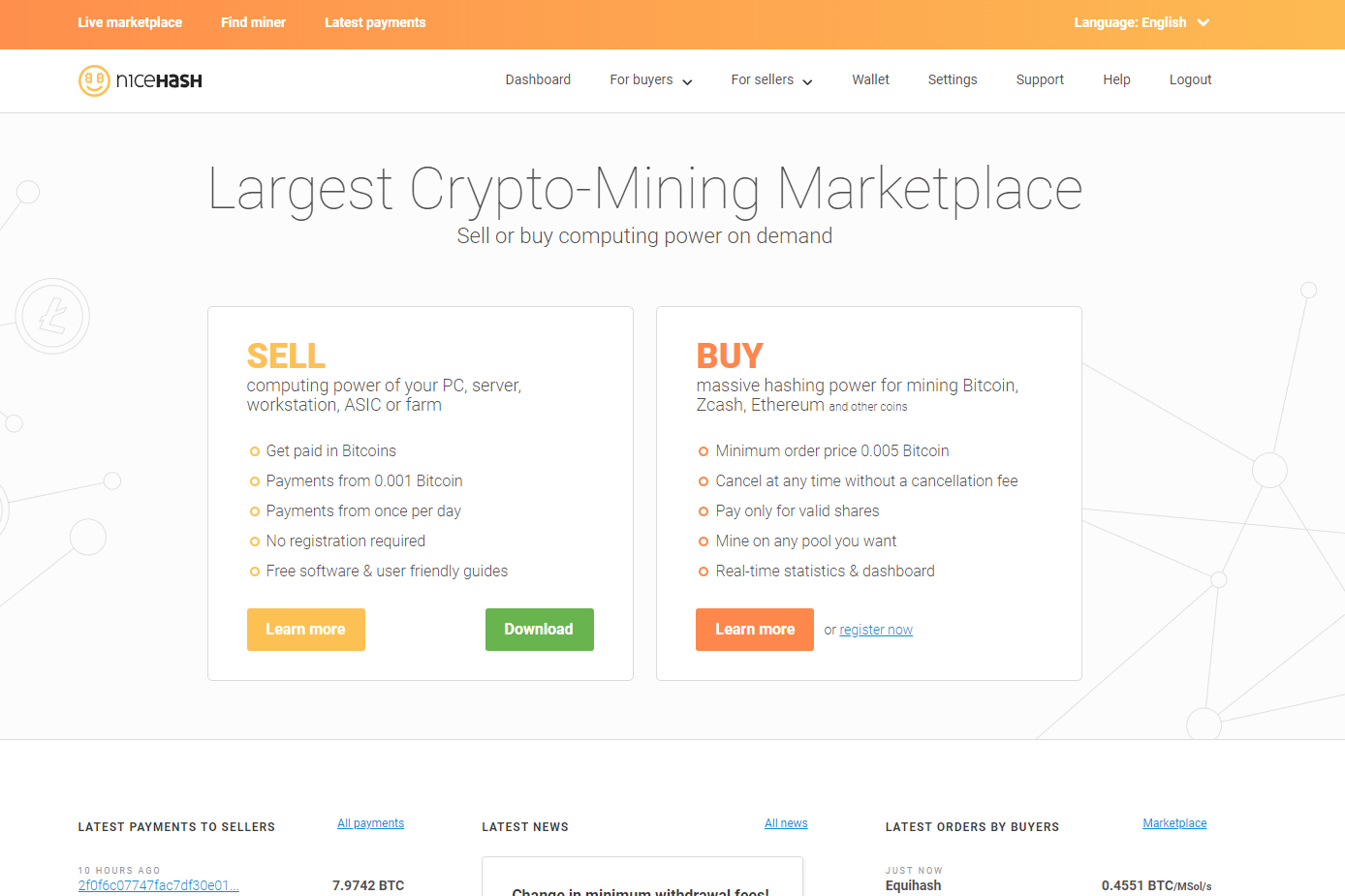

This time I’ve decided to cut to the chase and just use NiceHash, probably the most popular mining pool and supposedly the world’s ‘largest crypto-mining markeplace’. If I can’t make a profit there then I should probably just give up.

NiceHash Mining Marketplace Home Page (Image: BIUK)

Go to NiceHash.com and click on For sellers (with NiceHash you’re not directly mining, rather selling your mining power to other users to mine with). For a PC click on ‘I want to earn with my CPU or GPU‘. Download and install the NiceHash Miner software, choosing the version that’s appropriate for your graphics card.

When the software runs, accept the License Agreement and Risk Acknowledgement. It will then start setting itself up – note your virus scanner may give a warning (and even quarantine some files) so be ready for that; you may need to restart the installation if it appears to hang.

NiceHash Miner setting up (Image: BIUK)

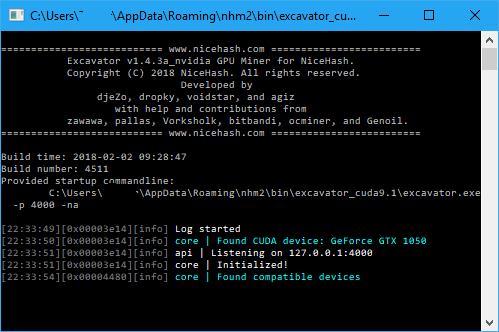

The miner launches a command window when it’s ready to run. It should show that it has found the graphics card and ‘initialized’.

NiceHash Miner command window (Image: BIUK)

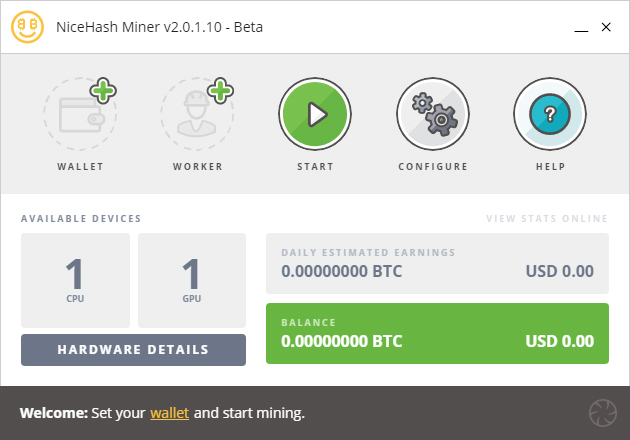

Once it is happy it will show its main screen ready to start:

NiceHash Miner ready screen (Image: BIUK)

Click on the link at the bottom to ‘Set your wallet‘. If you don’t already have an account at NiceHash you will need to create one. Registering for a new account is straightforward, you just click on the Create New Account to go to NiceHash, there you enter your email address and a password. Then you will need to setup the account (language, currency, create wallet, etc.).

Once done, enter the email address for the account into the NiceHash miner and click Save. The previous link will have changed to ‘Benchmark your devices‘; click on it, then the Benchmark All button and the Standard button.

The miner will benchmark and optimise for your system; this took just over 10 minutes on my PC. When it’s done click back to the main screen and click on the Start button. The status will change to Active – Running and mining is underway. The amount earned so far will show as Balance and the amount you are predicted to earn per day is shown as Daily Estimated Earnings (about £1 for this system).

Clicking on View Stats Online will take you to your account on NiceHash.com to show you more details, including your total earnings so far (the current Balance on the app is reset each time you start it). The overview there is particularly useful if you have more than one PC mining at the same time.

I’ve just set the system running and will check in an hour to see the result. What’s impressive is how quiet it is running – there must be scope to overclock it significantly. To get a better idea of what’s going on I’ve run up MSI Afterburner as recommended before.

Here I can see that the GPU is running at a temperature of just 65 degrees C – hardly working at all though it’s at 100% usage – and the CPU is likewise at about 60 degrees. Again this implies lots of opportunities for overclocking.

It’s now been running for an hour and it has earned 0.000004 BTC, worth about 3.2p. Energy usage by the PC has been 0.2 kWh, costing about 2.8p so it’s made a profit of 0.4p in an hour. That’s equivalent to about 10p per day.

It’s not a great deal of money – but at least it’s a profit!

This time the benchmark score was 1998 with a message “You can make an extra 100 USD per year with only this computer” – both values being roughly double what they had been before the upgrade.

MinerGate’s benchmark on a GTX 1050 system (Image: BIUK)

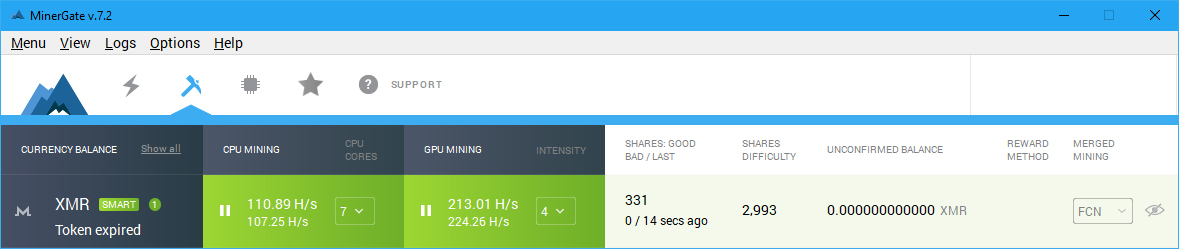

For the best outcome I set the mining to use both the CPU and the GPU (graphics card). This produced about 3 times as much hashing power as before.

Mining XMR using the MinerGate app and a GXT 1050 card (Image: BIUK)

However, given the poor results from last time (about 15p of Monero/XMR mined for 50p in costs) it’s clear that even at 3 times the mining power it would still not be very profitable. This is therefore another dead end.

The graphics card in my home PC died recently, probably related to me leaving the PC overnight which I don’t usually do (I guess it overheated). I woke to find that Windows had seen an error on it and uninstalled the driver, running it as a basic VGA card. I couldn’t fix it.

Anyway, I took the opportunity to buy a new mid-range graphics card, an Nvidia GTX 1050, to do some more experimenting with crypto mining. I didn’t want to go for a high-end (i.e. expensive) card since I have no plans to leave my PC running most of the time, or even to be mining while I was working at the PC, so a high-end card would likely never make its cost back.

A mid-range card, though, seemed like a good compromise – I needed a new card anyway, I could do some crypto experimenting, and I would get a benefit whenever I played 3D games. I settled on an EVGA card from Scan Computers as it was the cheapest version of the 1050 available – just £120 for a pretty powerful card.

Most impressive was that it didn’t need any additional power connectors to run, just making do with the power available from the motherboard slot. That implied it would use very little power – whereas the old (and relatively speaking slow) card it replaced had been using two additional power connections.

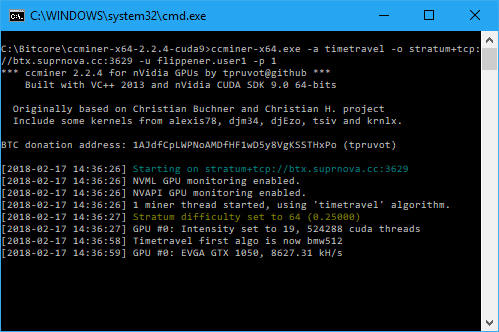

As an initial experiment I have rerun the test I did back last November using the GPU to mine for Bitcore. The procedure was much as described before (particularly following the embedded video) but with a couple of changes. Firstly, the mining app is no longer available on the Bitcore website so I downloaded it directly from the CCMiner code site. Secondly the batch file format has changed – however the download included a new Bitcore batch file so I used that, edited to include my Suprnova details as per the original post.

When CCMiner ran up the results were encouraging, showing a hash rate (mining power) of 8600 kH/s (8.6 MH/s), compared to about 1500 for the previous card.

CCMIner starting up on a GTX 1050 GPU (Image: BIUK)

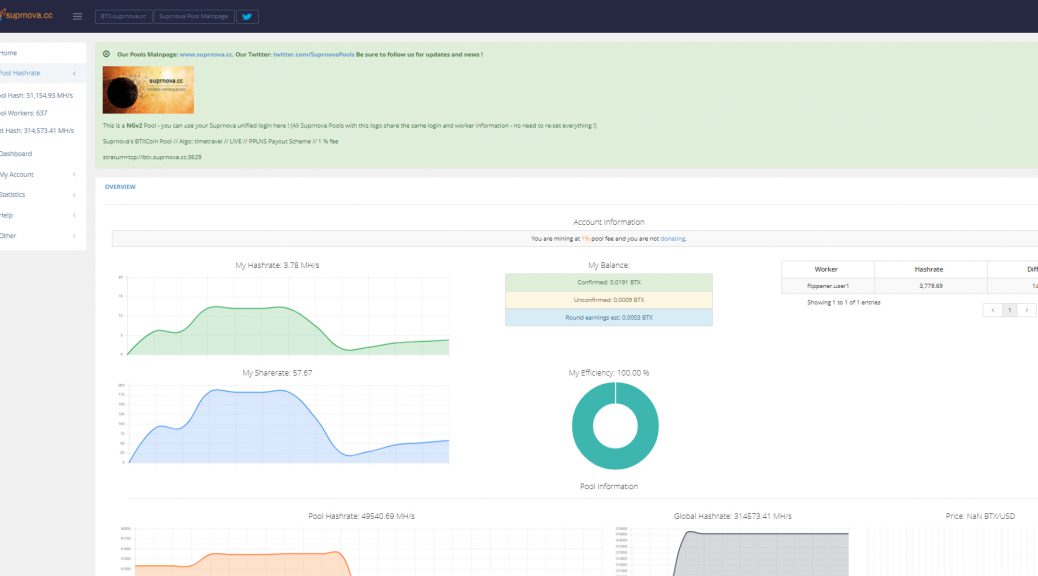

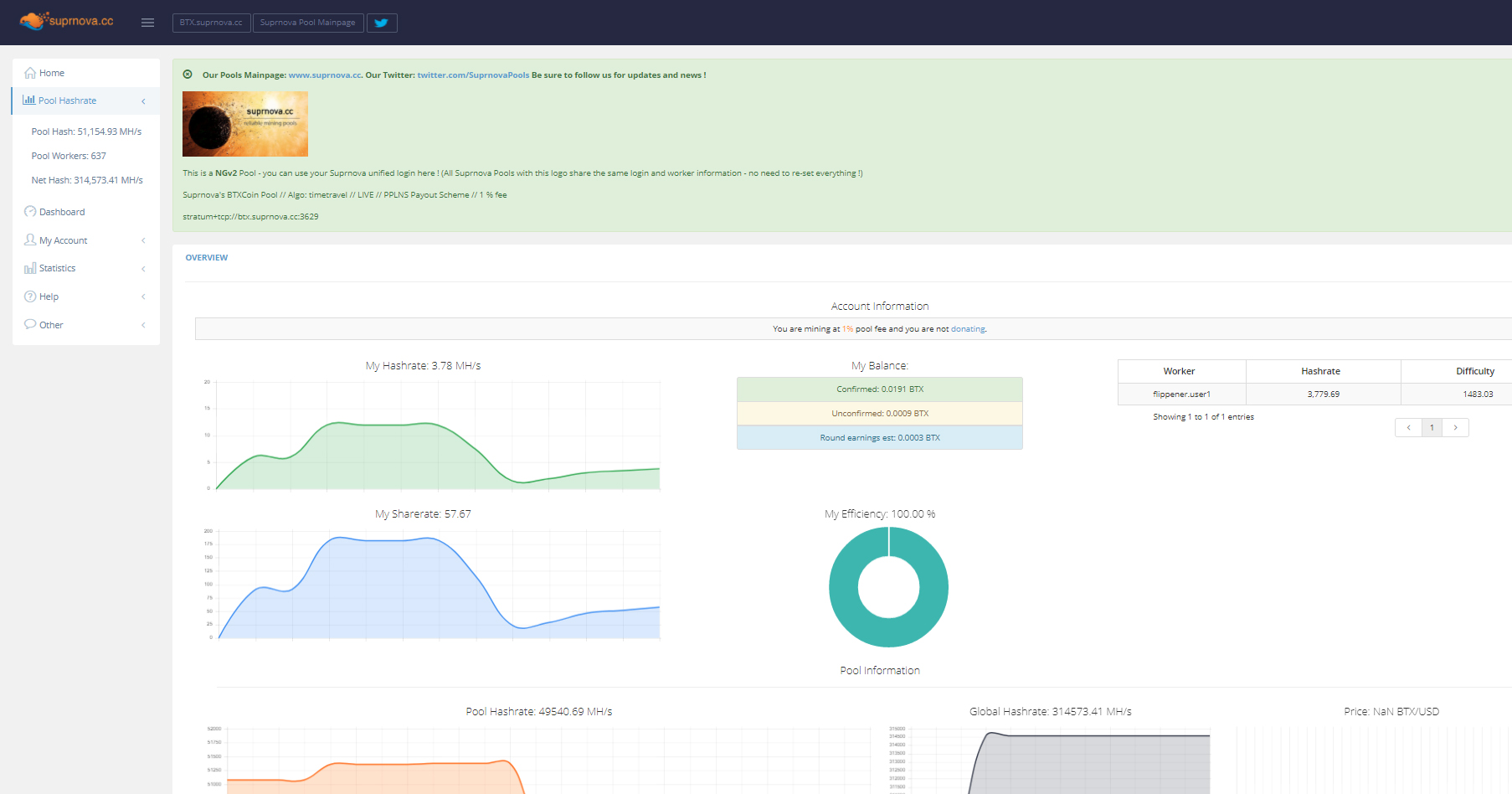

Running CCMiner for two hours produced 0.0018 BTX, according to my Suprnova dashboard, worth currently about 4p (the equivalent of about 50p per day). The PC was using about 150W with the card running and 85W without, so the card was drawing 65W – or 0.13kWh for the two hours. At my evening rate of 14p/kWh that means the mining cost me about 2p.

Suprnova Dashboard while running a GTX 1050 (Image: BIUK)

So – unlike last time – mining with this card is actually profitable, though only at the rate of about 1p per hour. What was more impressive, however, was how it did it.

Firstly, the energy use by the card was much less than the old card even though it was much more powerful, and it was very quiet. Secondly, it appeared to be truly mining ‘in the background’ with no apparent slowness caused to the PC while using it for other things. So it could make a profit, with little downside to having it running in the background virtually all the time. Taken together, it would seem that there’s plenty of scope to overclock the card to improve the performance.

Nonetheless, the bottom line is that this approach is not going to make a great deal of money, so I’m moving on to try other mining methods.