News outlets haven’t even had 24 hours to let the “10K” news simmer and it already climbed to $11,500. By the time they published the “11K” piece, it already dropped back to $9,000. Then, as soon as they entered the last word on their “Bitcoin is crashing!” article, it’s back at $11,000 per BTC.

Bitcoin (Image: Pixabay)

Amazing! But this is not unprecedented.

We’ve seen this before, back in 2013, a media frenzy when Bitcoin was approaching $1,000 that fueled that year’s bubble. In January of that year, one bitcoin was trading at around $15.00, rocketed to $266 by April, and then crashed back to $50 really quick. By November, it had already broken $1,000, peaking at $1,242 on Mt.Gox. That’s an almost 100-fold increase in 11 months, an order of magnitude larger than this year’s (2017) 10-fold run up.

Funny thing is, the charts then are almost identical to the ones today, and news articles look exactly the same. Just add one zero.

The media gobbles this up because people are fascinated by this stuff. Stories of people finding 5000 BTC in an old hard drive that they bought for $25 in 2009, a man throwing away 7500 BTC by accident and scouring a landfill to try and find it, a man buying pizzas for 10,000 BTC?—?It’s the sizzle to the steak and it sells.

The Other Side

People love it when things go up, but what goes up must come down, and Bitcoin is not immune to this. History shows three major “Bitcoin Bubbles”, and a LOT of volatility in between. Swings of 20–30% in one day are not uncommon in the Bitcoin world, but to most people this can be quite terrifying. For example, in the same day when Bitcoin broke $11,500 a couple of days ago, Bitcoin crashed back to $9,600, and lost 20% of its value overnight.

It isn’t just that, there are more. There’s that time it crashed from $260 to $50. Bitcoin was declared dead.

This was not what I expected to be doing with my October. But there I was, on a flight to Hong Kong, hoping I would be able to retrieve $200,000 worth of bitcoin from a broken laptop.

Four years ago, I was living in Hong Kong when a fellow journalist named Mike and I decided to invest in bitcoin. I bought four while Mike went in for 40; I spent about $2,000 while he put in $15,000. At the time, it seemed super speculative, but over the years, bitcoin surged and Mike seemed downright prescient. I had since relocated to Los Angeles and had been texting Mike about the 2,000 percent rise in our investment.

Strangely, I wasn’t getting much of a response from him. He had 10 times as many bitcoins as I did — shouldn’t he at least have been excited? Finally, when the price of one bitcoin broke $4,000 this summer, I sent him this message: “You do still have those bitcoins right?” That’s when he broke it to me: “Maybe not …”

Here’s what happened: At some point in 2013, Mike had rightfully become concerned about security. He initially kept his coins in an exchange called LocalBitcoins. Exchanges are commonly used to buy and sell cryptocurrency, but you shouldn’t keep your coins there. The most infamous bitcoin scandal to date was when Mt. Gox, an exchange based in Japan, lost 850,000 of its users’ bitcoins.

Exchanges can also suddenly close, as some did in China this year when the Chinese government suddenly made them illegal. Any serious cryptocurrency investor will tell you that your coins are best kept in “cold storage” (an offline hardware wallet). That’s what I’d done with mine, but Mike hadn’t gone that far three years ago when he started thinking about security. Instead, he set up a software wallet. It was a good step, but he would soon learn, it was not foolproof.

Super Bitcoin, Bitcoin Platinum, Bitcoin Uranium, Bitcoin Cash Plus, and Bitcoin Silver could threaten the Bitcoin ecosystem.

As Bitcoin continues its rapid journey to unprecedented heights, the plot thickens: at least three Bitcoin forks have been scheduled for the month of December, with more to follow in January, February, and March of 2018. Bitcoinist questioned if the sudden rash of Bitcoin forks was “the dawn of the ‘initial fork offering’”.

Bitcoin Fork Pens (Image: BTC Keychain/Flickr)

Super Bitcoin, Bitcoin Cash Plus, Bitcoin Silver, Bitcoin Platinum, and Bitcoin Uranium (which has the quaint ticker symbol ‘BUM’) are all on the menu. Each of these coins claims in its own way to solve the issues of scalability and centralization that have plagued the Bitcoin network, although none of them really seem to have proven that they have the technological basis to do so.

For example, Bitcoin Silver (BTCS), which claims to be making “cryptocurrency accessible to the rest of the world”, claims to have an “incredible team consisting of financial experts, blockchain developers, telecommunication influencers, international law experts, and local business ventures” that are based all over the world. However, none of the identities of any of these supposed team members are anywhere to be found.

A pillar analysis of the market shows a promising future for cryptocurrency, despite the naysayers.

One of the biggest hurdles bitcoin has faced throughout 2017 has been poor journalism around the cryptocurrency, along with uneducated opinions from many so-called “experts” within the financial industry.

Jamie Dimon famously labelled the currency a “fraud” suitable for murders and drug dealers, while the chief economic advisor of Allianz said in September it should be worth half of what it was trading at back in September when it was edging US$5,000. I wrote about this in my last article when the price fell back to US$3,600.

Peter Switzer, a prominent and well respected financial commentator, was asked for his thoughts on the cryptocurrency around the same time in September. However in a more honest approach he advised he had chosen not to invest stating “I subscribe to the view that I don’t invest in things that I don’t understand”, further quoting Charlie Aitken’s reference to bitcoin being a “bubble”.

Bitcoin price chart (Image: geralt/Pixabay)

The real negligence here has come into play, as there have been few signs that many of the most prominent financial commentators actually understand the cryptocurrency. Myopia has hit many individuals we have historically trusted to understand financial markets.

Despite the numerous comparisons, the cryptocurrency boom displays very few characteristics to Tulip Mania outside of a huge price spike. Many more similarities are found in comparison to the oil rush in the 1850’s, which was actually the largest wealth transfer of this magnitude prior to the evolution of cryptocurrency. Those involved in it simply understood that the world was moving away from the horse and cart, and into a realm where oil would become an essential pillar of the economy. In the same way, currencies are changing and they are about to have a profound impact on everyday life.

It’s time those around the financial industry, especially those giving financial advice and opinion, actually understood the currency, and what its technology really means for the future of currencies.

After all, what was going on with Bitcoin in the last few months?

It looks like, in the last few months, Bitcoin has made friends with forking. When I wrote about Bitcoin forking the last time, I didn’t expect there would be this many so soon. But hey, here we are, trying to make sense of what the hell is happening in the crypto world.

Bitcoin fork pen and bitcoin keychains (Image: BTC Keychain/Flickr)

With this article, I try to put everything that has happened since Bitcoin Cash in a proper order that would become anyone’s go-to article for learning about Bitcoin forks between August 2017 and November 2017.

🍴 But first, what is a fork?

“You don’t need a silver fork to eat good food.”?—?Paul Prudhomme

You can think of blockchain ledger as a stack of pages. Every full node in the network keep a copy of this stack of pages with themselves. Everyone’s copy of the ledger is exactly the same because everyone followed the same set of rules to build it.

So, if there are ten people in the network, each of them will have a copy of the ledger that would look something like this:

Mining cryptocoins is an arms race that rewards early adopters. You might have heard of Bitcoin, the first decentralized cryptocurrency that was released in early 2009. Similar digital currencies have crept into the worldwide market since then, including a spin-off from Bitcoin called Bitcoin Cash. You can get in on the cryptocurrency rush if you take the time to learn the basics properly.

Which Alt-Coins Should Be Mined?

If you had started mining Bitcoins back in 2009, you could have earned thousands of dollars by now.

At the same time, there are plenty of ways you could have lost money, too. Bitcoins are not a good choice for beginning miners who work on a small scale. The current up-front investment and maintenance costs, not to mention the sheer mathematical difficulty of the process, just doesn’t make it profitable for consumer-level hardware. Now, Bitcoin mining is reserved for large-scale operations only.

Bitcoin mining (Image: Pixabay)

Litecoins, Dogecoins, and Feathercoins, on the other hand, are three Scrypt-based cryptocurrencies that are the best cost-benefit for beginners. At the current value of Litecoin, a person might earn anywhere from 50 cents to 10 dollars per day using consumer level mining hardware.

Dogecoins and Feathercoins would yield slightly less profit with the same mining hardware but are becoming more popular daily. Peercoins, too, can also be a reasonably decent return on your investment of time and energy.

As more people join the cryptocoin rush, your choice could get more difficult to mine because more expensive hardware will be required to to discover coins. You will be forced to either invest heavily if you want to stay mining that coin, or you will want to take your earnings and switch to an easier cryptocoin.

Like everyone involved in cryptocurrency I know that Bitcoin and other coins are produced through mining:

Bitcoin mining is the process by which transactions are verified and added to the public ledger, known as the block chain, and also the means through which new bitcoin are released. Anyone with access to the internet and suitable hardware can participate in mining. The mining process involves compiling recent transactions into blocks and trying to solve a computationally difficult puzzle. The participant who first solves the puzzle gets to place the next block on the block chain and claim the rewards. The rewards, which incentivize mining, are both the transaction fees associated with the transactions compiled in the block as well as newly released bitcoin.

I also know that in most cases Bitcoin mining is done by big organisations, mostly in China and Eastern Europe, running large farms of mining computers. It’s tough to compete against that.

Cryptocurrency Mining Farm (Image: M. Krohn/Wikimedia)

However, in learning about my current ‘favourite’ coin, Bitcore (BTX), I found out that it can be mined on a home PC with a half-decent graphics card. I decided to give it a go.

The basic process is straightforward:

You run a dedicated mining app, typically CCMiner, which mines Bitcore by maxing out your graphics card.

You connect the app to an online mining pool server so your mining power contributes to a pool of other miners’ hardware and you share the coins created. I use Suprnova.cc.

You connect your mining pool account to your Bitcore wallet so that payouts come to you.

The details are covered well in a YouTube video by Mod Rage, ‘How to Mine Bitcore (BTX) for Beginners (From Scratch)‘, included below. There’s another one that gives some additional useful information by IMineBlocks.

https://www.youtube.com/watch?v=Dw6CuHD-Ca8

My Setup

When I initially tried running CCMiner I got the error “qubit_luffa512_cpu_init” each time. I worked out this indicated my graphics card was too old to run the latest version of CCMiner – no great surprise there – so I went back through older versions to find one that worked for me. That turned out to be the x64 version of build CCMiner v2.2.

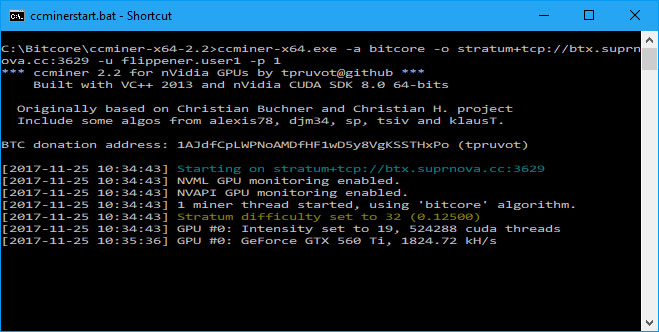

When you start up the miner, initially not a lot happens – you just get a command window with a basic startup screen:

CC Miner Screen – startup (Image: BIUK)

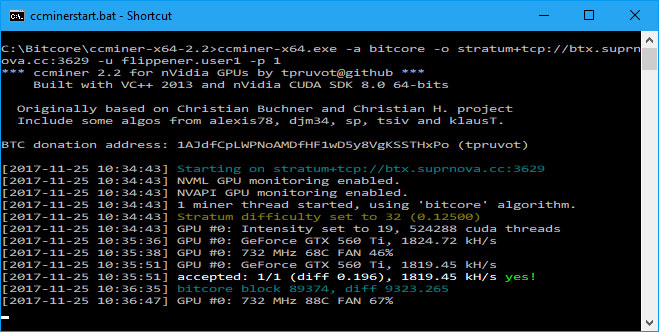

After a minute or two, however, you will likely become aware of a rising background noise as your graphics card starts to ‘take off’. You may also find your PC’s response becomes a bit ‘sluggish’. Here mine has started – the card temperature has increased from 68C to 88C, and the fan speed from 46% to 67%:

CC Miner Screen – startup 2 (Image: BIUK)

The key thing is the “yes!” message which tells us it has started to mine successfully (failure is indicated by “boo!”). Success seems to improve over time, so initially I only get occasional successes:

CC Miner Screen – early on (Image: BIUK)

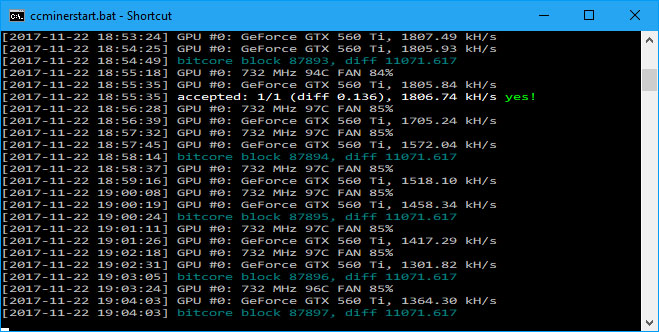

But half an hour or so after starting up each time I see screens like this – we’re up and running (the card settles at a temperature of about 95C and a fan speed of about 85%):

CC Miner Screen – up and running (Image: BIUK)

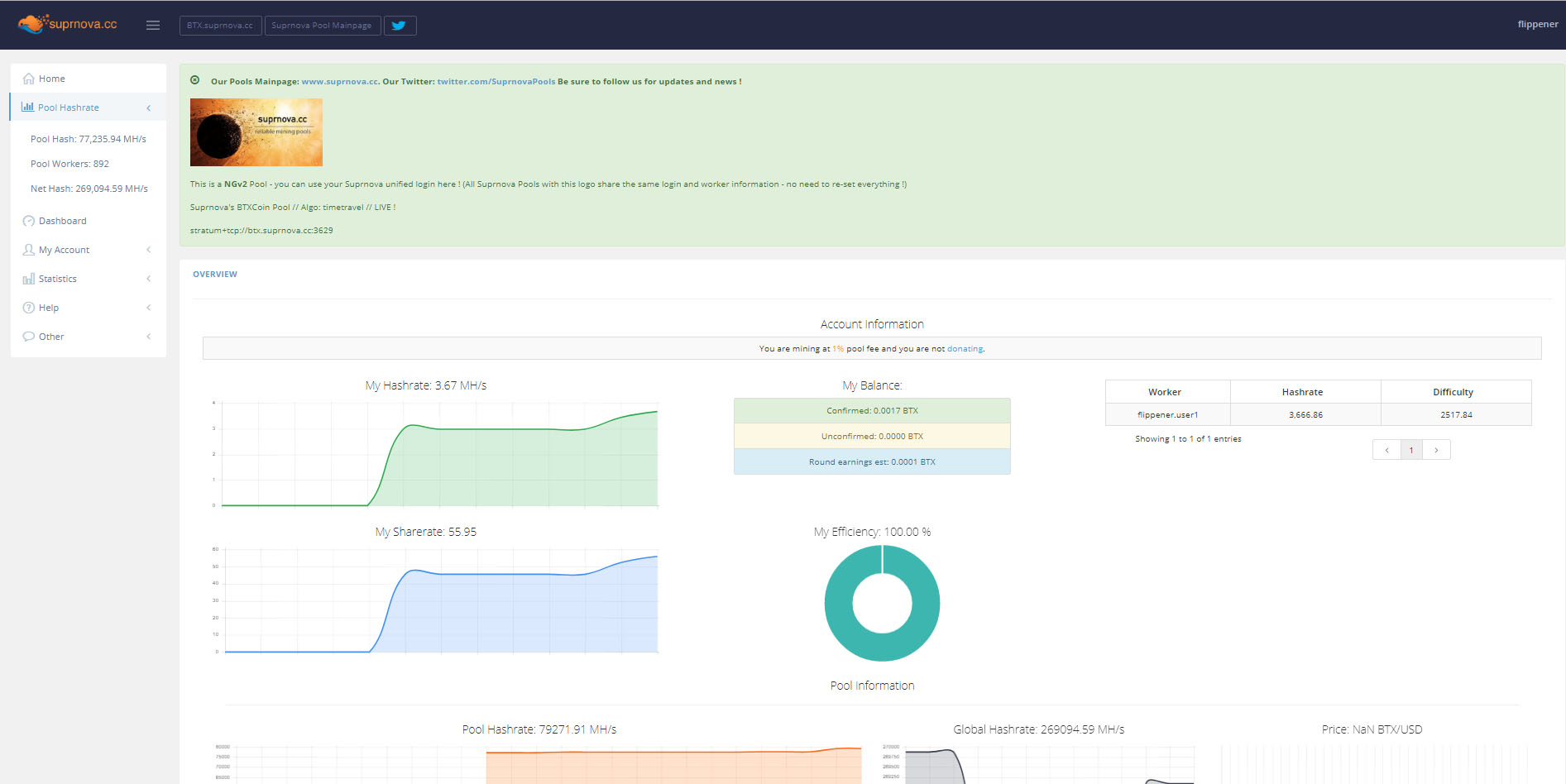

In parallel we can monitor the status on the Suprnova website – this shows us in approximate real-time how much solving power (‘hashrate’) we are contributing to the pool, for example:

Suprnova Status screen (Image: BIUK)

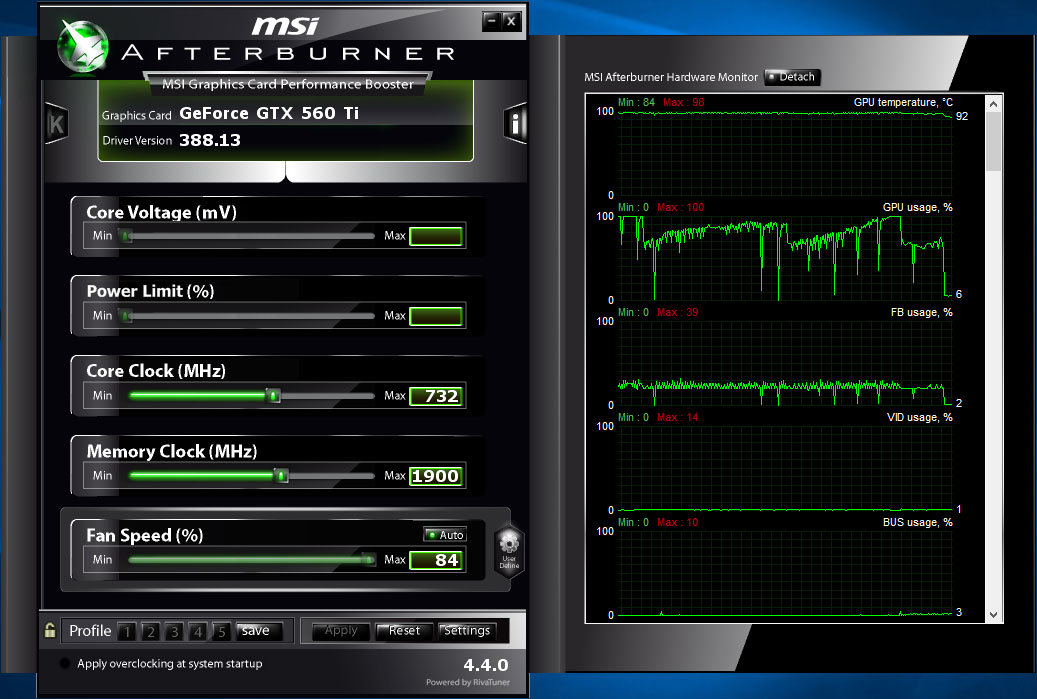

To monitor the graphics card itself, which of course is now running hot, you can use various utilities. Probably the best known is MSI Afterburner – here it is (with its UI skin set to ‘Default MSI Afterburner v3 – big edition’) showing a real-time display of card temperature and Graphics Processing Unit (GPU) usage:

Afterburner Status screen (Image: BIUK)

The GPU usage varies over time, but if I stop using the PC for other things it starts to settle near 100% as you would expect.

Mining Results

So is Bitcore mining profitable with my setup? I decided to work it out over the course of an evening, specifically a 5 hour period.

First I used a watt meter to work out how much energy the PC consumed. This turned out to be about 240W when mining and about 180W when not mining, so about 25% of the electricity used in that period was used for mining.

The watt meter told me I had used 1.25kWh over the period so about 0.3kWh was used for mining. My evening electricity rate is about 14p/kWh so the mining cost me about 4p.

So how much did I earn? Suprnova tells me I mined about 0.0006 BTX, which is worth somewhere around 2p. So no, my setup isn’t profitable as I ran it.

Can Bitcore Mining Be Profitable?

The result is interesting to me because, actually, it’s not as bad as I feared. After all, I am running an old PC with a graphics card that is old enough it can’t run the latest – and presumably most efficient – mining software.

(Tip: you can look up the power, ‘Compute Capability’, of your Nvidia card here. A good value is 6+, mine – a 1Gb NVIDIA GeForce GTX 560 Ti – is 2.1).

With the current setup I could:

Run only at night, leaving the PC mining on Economy 7 electricity and unattended (which should get the efficiency up by 10%-15%). My overnight rate is about half the daytime rate so immediately I would be close to breaking even, and maybe even making a profit.

Run only during the middle part of the day, with the PC mining just on electricity from my solar panels. It would immediately become profitable, even if only at the rate of a few pence per day. And that’s without even trying overclocking on the card.

Of course, if I really want to mine seriously I would be looking at buying new hardware – specifically a powerful graphics card, as it’s not necessarily an issue if the PC isn’t particularly fast.

Initial research implies that a current top-end graphics card may have enough power (hashrate) to mine at perhaps 30 times the rate of my current card. Suddenly Bitcore mining starts to become a realistic proposition – a profit of £1-2 per day seems achievable – so I’m going to investigate further.

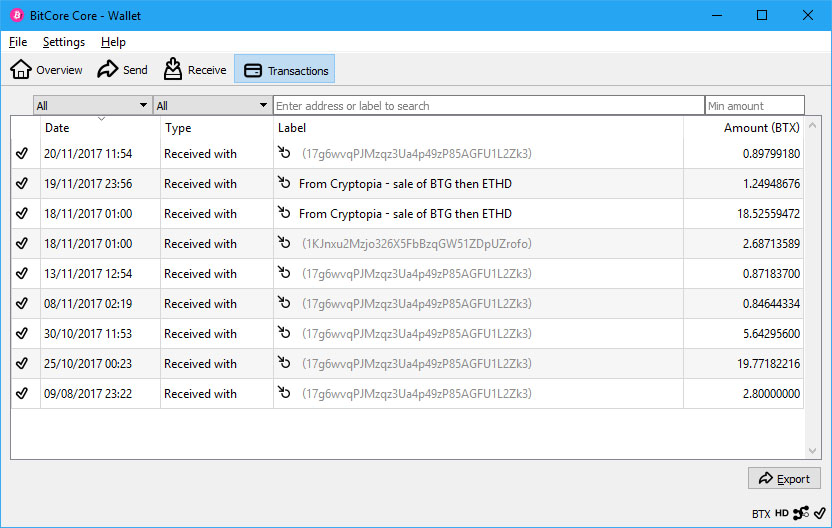

November has been a lively month in cryptocurrency, but particularly for the Bitcore coin (symbol BTX). I’ve written a number of blog posts about it, but I think a summary would be worthwhile:

1. One month ago, on 22 October, I had just 2.8 Bitcore, courtesy of a free airdrop from last April. Each Bitcore was worth about $6 so the total value was about £13.

2. To get the next big Airdrop I needed to own at least 10 Bitcore, so I decided to simply buy £100 worth on 25 October. That got me 19.77 BTX, for a total of 22.6 BTX. With Bitcore at about $7 that was worth about £120.

3. Having met the threshold I received a one-off airdrop of 25% on 30 October bringing the total to 28.2 BTX, at about $8 each, so a total of £170.

4. While the one-off airdrop was nice I was actually after the weekly 3% airdrops and the first one came in on 8 November. At this point I reached 29 BTX at about $10 each so worth £227.

5. The next weekly airdrop on 13 November took me to 30 BTX at $13, so £290. This was starting to look serious!

6. On 18 November I received my Bitcoin Gold airdrop. Since Bitcore was doing so well I used the money to buy some more. Bitcore had another airdrop of their own so my end result was 51 BTX, now at an impressive $30, so worth £1100!

7. The next day I sold a small Ethereum Dark airdrop for 1.25 more BTX.

8. This Monday the next weekly airdrop came in giving me another 0.9 BT

The end result for the month – not counting at least another weekly airdrop to come in before the end of this month – is that I now have 53.3 BTX. Today their value has dropped back a little to $27 each, so their total value still hovers around £1100.

Bitcore November transactions (Image: BIUK)

So, through a whole series of free airdrops, plus a big rise in the market, my outlay of £100 is now worth £1100. Just one reason why I love cryptocurrency!

To an extent it feels like I’ve earned the money, by ‘jumping through hoops’ to claim the free airdrops. Therefore the outcome is the most satisfying, despite the fact that over the same month, by doing nothing, each of my Bitcoins (BTC) has gone up in value from £4100 to £6200, so my 12.5 BTC have gone up by an astonishing £26,000 in a month. Somehow that seems less real than the BTX gains.

I’m a bit of a fan of Bitcore (BTX) as is clear from my BTX blogging history – largely, I confess, because it has so many airdrops! Who doesn’t like free coins?!

Airdrop (Image: NMUSAF/Wikimedia)

Less than a week after the last 25% airdrop on 30 October (based on how many BTX you own), there was another airdrop on 2 November (based on how many Bitcoin/BTC you own) – both taking place in parallel with the weekly 3% airdrops. It’s raining free Bitcore coins!

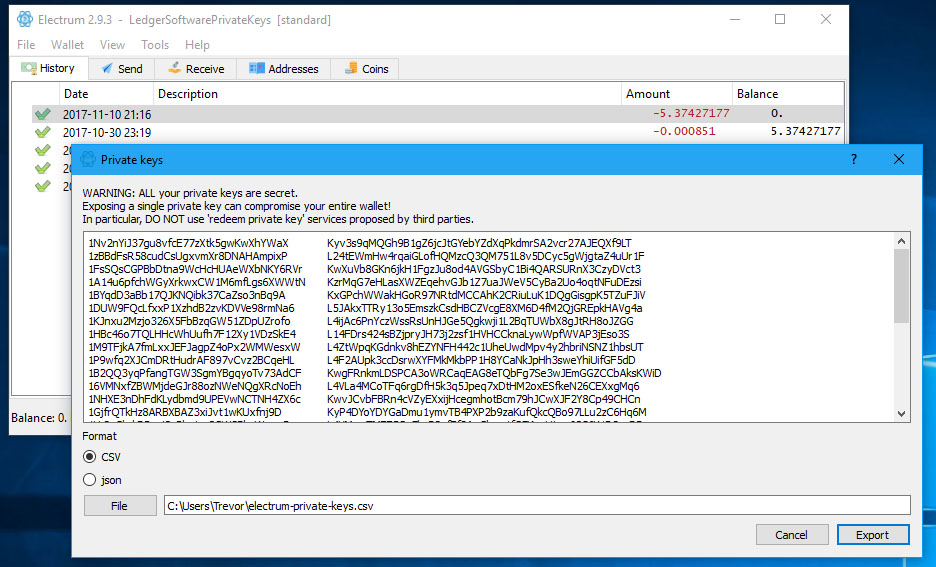

However, getting the private key to your BTC account as required by that description can be tricky, so here I’ll explain how to do it if you’re holding your Bitcoin in Electrum as per my previous posts.

To be eligible you need to have held Bitcoin on 2nd November in a wallet you control, i.e. one to which you have the private keys, and you will get 1 BTX for each 2 BTC. Log into your Electrum Wallet go to Wallet -> Private Keys -> Export, then enter your password and wait a few moments. Look for the address containing your Bitcoin in the left column and copy the private key from that right column:

Electrum Export Private Keys screen (Image: BIUK)

It’s this key that you paste into the Bitcore Wallet console as described in the Steemit description linked above. Note, as ever, as soon as you have exposed a private key you may have compromised your wallet security (you can see in the screenshot to be safe I had already moved out my Bitcoin from the wallet before making the claim). At this point, if you want to be completely safe, you should wipe the wallet before using it again.

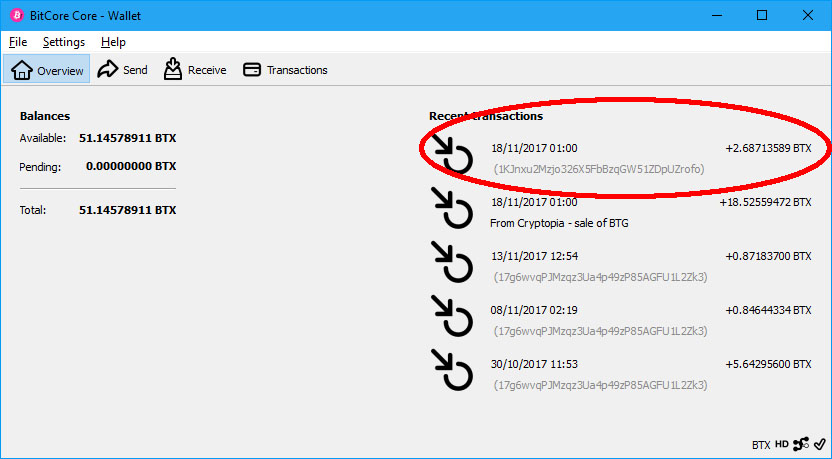

Anyway, that’s it done – the new BTX should appear in your Bitcore Wallet straight away if it works, otherwise check that you used the correct location address for your BTC on 2nd November.

It worked for me – my 5.8 BTC gave me 2.7 more BTX, so in total currently worth about $50/£40 – not a bad freebie!

Bitcore 2nd Snapshot (Image: BIUK)

The leading Bitcoin and Cryptocurrency site for UK investors