As Bitcoin and cryptocurrencies gain more and more media coverage, investors who have never been involved in crypto are increasingly asking the question of whether cryptocurrencies could provide meaningful portfolio diversification to the traditional portfolio asset allocation.

In order to answer this question one must look both backwards and forwards: backward looking to determine past correlations and risk-reward profile; and forward looking to understand the real risk of central bank policy mistakes and government debasement of fiat currencies.

Open bank vault (Image: ahobbit/Pixabay)

Diversification of portfolio focuses on how the volatility of an underlying security plus their correlation with core market assets impacts a portfolio’s risk-return characteristics over the long-term or during periods of extreme macroeconomic or market stress.

Diversification drivers

The main reasons why Bitcoin provides portfolio diversification are: investability, politico- economic features, correlation of returns, and risk-reward profile.

Google will ban all cryptocurrency-related advertising of all types in June 2018, according to a recent update to their Financial Services policy.

The news of a crypto ad ban comes just days after crypto advertisers using Google Adwords noticed a drastic drop in the number of views of their advertisements, according to posts on the Adwords support pages. However, Google Adwords had at that time denied any change in their Financial Services regulations that would block cryptocurrency or Initial Coin Offering (ICO) related advertisements.

Cryptocurrency Art Gallery: Litecoin, Ether, Ripple, Bitcoin and Namecoin (Image: Namecoin/Flickr)

Under Google’s newly updated financial products policy, no advertisements for “cryptocurrencies and related content (including but not limited to initial coin offerings, cryptocurrency exchanges, cryptocurrency wallets, and cryptocurrency trading advice),” will be accepted.

A state employee at Florida’s Department of Citrus (FDoC) has been arrested for allegedly using official computers to mine cryptocurrencies.

According to the Tampa Bay Times, the Florida Department of Law Enforcement (FDLE) has jailed Matthew McDermott, IT manager for the state government agency that oversees Florida’s citrus industry. He is reportedly being held pending trial, with bail set at $5,000.

Cryptocurrency Mining Farm (Image: M. Krohn/Wikimedia)

The FDLE alleges that McDermott used computers in the department to mine cryptocurrencies including bitcoin and litecoin, and has charged him with grand theft and official misconduct, according to the report.

An investigation further indicated that the utility bill of the department had surged by over 40 percent from October 2017 to January 2018, as cryptocurrency mining requires significant amounts of electricity due to its high processing demands.

This evening I attended an interesting lecture on Blockchain at the University of Northampton, presented by Drs Ali Al-Sherbaz and Scott Turner. It covered the basics of blockchain, include hashing, mining, signing, creating blocks, and so on.

It then covered particular examples of blockchain projects within the University, including one on social interactions and one on network activity logging. Apparently Blockchain is one of the key topics the University will be addressing in its future development strategy.

What wasn’t covered, however, was Bitcoin and in general most comments were dismissive of cryptocurrency. I think that will prove to be shortsighted. Most of the criticisms and limitations levelled at Bitcoin and other cryptocurrencies during the event were demonstrably false or at least incomplete and a more detailed discussion would have demonstrated that.

Personally I think cryptocurrencies are here to stay, with Bitcoin taking the role of the reserve cryptocurrency, and their positions will get stronger and stronger over time. Whether they will eventually replace fiat currencies is less clear, but I certainly wouldn’t dismiss the possibility.

Proof of Work (PoW) mining operations, like Bitcoin and Ethereum, use a tremendous amount of energy and generate a tremendous amount of waste heat.

Qarnot is one of a number of growing companies that has found a way to turn that waste heat into controlled heating for the home or office.

The new Qarnot QC-1 “crypto heater” takes advantage of an obvious synergy: It makes use of the waste heat generated by mining crypto in the guise of an attractive space heater.

Qarnot Crypto Mining Heater (Image: Qarnot)

Spec wise, the QC-1 contains two GPUs: NITRO+ RADEON RX 580 8G 60 MH/s at 650W. Local electrical costs and climate are key determining factors with regard to recouping costs and making a profit; for example, if you are in a cold northern environment with cheap electricity like Quebec, then your costs to run it should be low enough (about $0.03 KWh USD) that the mining revenue should pay for the device in a few years.

The device mines Ethereum by default but can be configured to mine various other PoW-based cryptocurrencies such as Litecoin. A mobile app is available to monitor your account and configure the unit. The lack of fans or hard drives leads Qarnot to claim the system is “perfectly noiseless.”

The Australian Federal Police (AFP) are investigating two employees at the Bureau of Meteorology for allegedly using the bureau’s computers to mine cryptocurrencies, the Australian Broadcasting Corporation (ABC) reports today, March 8.

Bitcoin mining (Image: Pixabay)

The AFP appeared at the Bureau of Meteorology last week, Feb. 28, with a search warrant and questioned two IT employees, one of whom has since gone on leave. ABC reports that no charges have yet been filed, and both the AFP and the Bureau of Meteorology have declined to comment pending the ongoing investigation.

Bitcoin prices fell below $10,000 Thursday as a bear market reversed growth which saw BTC/USD achieve weekly highs of $11,675 March 5.

Price data from Coinmarketcap shows Bitcoin losing around $400 in three hours to hit $9658, recovering slightly to trade around $9900 at press time.

Bitcoin price chart (Image: geralt/Pixabay)

The behavior continues what has become a pattern for BTC/USD over the past month, with upticks towards $12,000 encountering resistance before diving below $10,000, then repeating the cycle.

As Cointelegraph reported previously, several analysts have warned that closing above $12,400 will be a decisive event for traders, but this will be difficult to achieve.

I was right about the Bitcoin Dip – and have made a tidy profit. I bought half a Bitcoin at £5500.

Of course, it should have cost me £2750 but I bought it through Coinbase with my debit card which is a pricey, though convenient, way to do it. Coinbase charged me 4%, so about £110, making the total £2850.

Bitcoin was been rising in value since as I predicted, though in its usual erratic way. I had intended to take my money out when it passed £8000 and, as I watched it last night, it did just that.

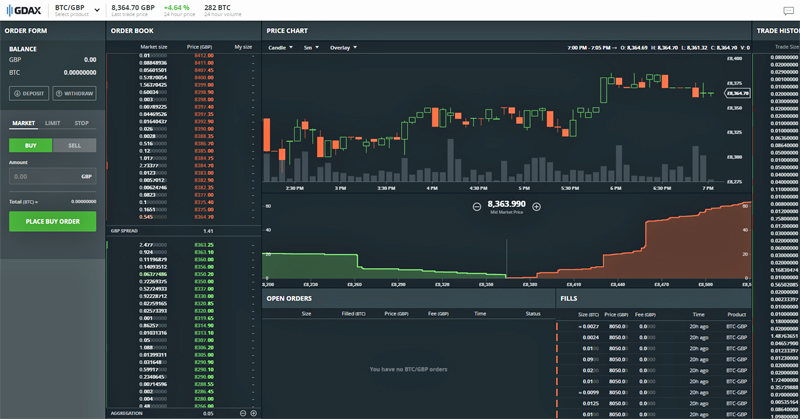

I was hesitant to sell it directly through Coinbase again because of its fees. However, I had come across some advice about selling through Coinbase’s exchange, GDAX, instead at lower fees. Here’s an example video from the excellent Coin Mastery:

I followed the advice and it worked like a charm.

GDAX Exchange Trading Screen (Image: BIUK)

This is the process if you want to save a stack on Coinbase fees:

Create a GDAX account if you don’t already have one (I already did).

Transfer the Bitcoin to GDAX – on GDAX click the DEPOSIT button, then in the form choose your Coinbase Account -> BTC Wallet and set the amount. Click Deposit Funds. It will appear almost immediately on GDAX and there is no charge.

Select LIMIT then SELL, then set the amount. Here you need to be a bit careful and set the correct price you are prepared to sell at (double check it, because if you set it low it will sell low). At the time Bitcoin was selling for about £8010. I wanted to make sure that, if there were fees, I would clear £4000 on my 0.5 BTC so I set the value to £8050.

Since the price is volatile your price will likely be hit very quickly so long as you didn’t set it too high (mine too less than a minute).

The BTC sells, the money appears in your GDAX wallet – and there’s no fee!

Transfer the money back to Coinbase using the WITHDRAW button, set the amount and the destination (e.g. GBP Wallet) and click WITHDRAW FUNDS. It goes back to Coinbase – no charge.

So I have proved to my own satisfaction you can sell BTC, i.e. convert it to pounds sterling, for no charge this way – and at a price slightly higher than the current market rate

Note that selling Bitcoin is called a ‘Maker’ transaction since you are putting Bitcoin into the market. Note that moving in the opposite direction has a ‘Taker’ fee of 0.25%, still not a bad deal.

I sold my 0.5BTC at £8050 so I received £4025, and that’s all now sitting in my Coinbase account.

Since I only paid £2870 for the Bitcoin less than a month ago (a profit of about £1100), I’m rather pleased with that.

After my initial experiments into mining for cryptocurrency with my own PC’s GPU and CPU, and even before acquiring my improved GPU, it was clear that good mining results were only possible with specialised and up-to-date hardware. Therefore about Christmas I ordered a new PC with a view to designing it for use in cryptocurrency mining.

We needed a new family PC for occasional use anyway (for children’s homework, etc.) as our previous one was old and had slowed down to the point it was almost useless. At the same time I knew it would be idle most of the time, when it could be used as a dedicated mining machine.

The Beast – High End Mining PC (Image: BIUK)

I took some time investigating the options before deciding on the specification I wanted. Although all our previous PCs had come from Dell, this time I ordered through Scan PC to get exactly what I wanted at an acceptable price:

A gaming motherboard with twin high speed GPU slots

A large, clear-airflow case with sound insulation

Two top-end GPUs – the NVidia GTX 1070 Ti

A high power (850W) power supply

High performance disks (an SSD for fast access, and a RAID array for backup)

The Beast – High End Mining PC (Image: BIUK)

In discussions with Scan I changed the spec a couple of times after ordering (e.g. increasing the memory) and was pretty happy with their service. It arrived in January and so far has shown itself to be a very powerful machine. It cost an eye-watering £2500, but then the two graphics cards alone were about £650 each.

I’ll blog about how I got on with it, including its mining capability, in the next few posts.

In January I completed and filed my 2016-2017 UK self-assessment tax return, for which I had to consider the tax implications of my cryptocurrency holding and trading. While I was able to convince myself that there were no issues for that period, since I had sold no cryptocurrency (only bought) in that period, it was clear that I would definitely need to consider tax in detail for the upcoming 2017-2018 period.

My first step, back last summer, was to invest in a cryptocurrency accounting app known as CoinTracking.info. I have used it carefully since to record all transactions, but nonetheless it was clear that while it could help with tax filing, it was necessary for me to research and understand the issues myself.

Bitcoin ‘Taxation is Theft’ (Image: Pixabay)

The tax situation in the UK for cryptocurrency is unclear so here I’m going to record my views on the current situation – if anyone knows otherwise, please detail any corrections in the comments.

In a nutshell for an individual (not a company) with a moderate amount of cryptocurrency (less than £45k) it is as follows:

Capital Gains Tax (CGT): If you buy and sell cryptocurrency then you are liable for capital gains tax on the difference in value of the currency between when you bought it and when you sold it, valued in pounds sterling. Where this exceeds the CGT tax-free allowance (£11,300 for 2017-18) there is tax to be paid.

Income Tax: If you trade or mine cryptocurrency then you are liable for income tax on the value of the currency gained, valued in pounds sterling. Where this exceeds the income tax personal allowance (£11,500 for 2017-18) there is tax to be paid.

Value Added Tax (VAT): In virtually all circumstances VAT can be ignored (as with most conventional currencies).

While the guidance suggest that on a case-by-case basis some cryptocurrency transactions may be considered to be gambling or betting – and therefore not taxable – I will assume that the safest course is to assume that, if reviewed, all transactions will turn out to be taxable on the basis just described.

Note that, in my opinion, income tax is probably liable on any free gains of cryptocurrency, for example:

With regard to CGT, it looks like cryptocurrency will be valued in the same way as shares. If you have bought and sold lots at different times then the value of what you sell compared to what you paid for it can be difficult to calculate – how do you match which sold Bitcoin to which bought Bitcoin?

Following HMRC guidance for shares the process is basically:

Same Day Rule: If you buy and sell on the same day then the coins can be matched off against each other (even though you bought and sold at different values) and there is no CGT liability. You just have to consider CGT on any ‘left over’, i.e. if you sold more than you bought.

Bed and Breakfasting Rule: Any coins not covered by the first rule but bought and sold within 30 days can be matched against each other, and CGT is due on the difference between the buying and selling values.

All others: Any coins not covered by the first and second rules are considered to be held in a single pot (called a ‘Section 104’) and when some are sold they are valued at their proportion to the value of the total pot. That value is determined by adding up the bought price of the coins in the pot.

That’s the tax situation for cryptocurrency as I understand it so far, though of course I will look into it further in time for my next tax return. With that return in mind, I have decided to do some specific bookkeeping in advance (probably in spreadsheets) and if you own crypto you might want to consider doing something similar:

Track the buying and selling of all crypto coins to pounds, with dates, in order to determine the CGT liability as per the 3 rules just described.

Track the receipt of any free coins (including airdrops, forks and faucets) in order to determine the income tax liability – even if (particularly if) the coins ended up in the same account as those that were paid for.

The leading Bitcoin and Cryptocurrency site for UK investors